Five Technological Trends Reshaping the Global Computing Chip Industry by 2025

02/19 2025

02/19 2025

501

501

Produced by Zhineng Zhixin

Artificial Intelligence (AI) has emerged as a pivotal force propelling the entire industry forward, particularly through its widespread adoption in data centers, edge computing, and the Internet of Things (IoT).

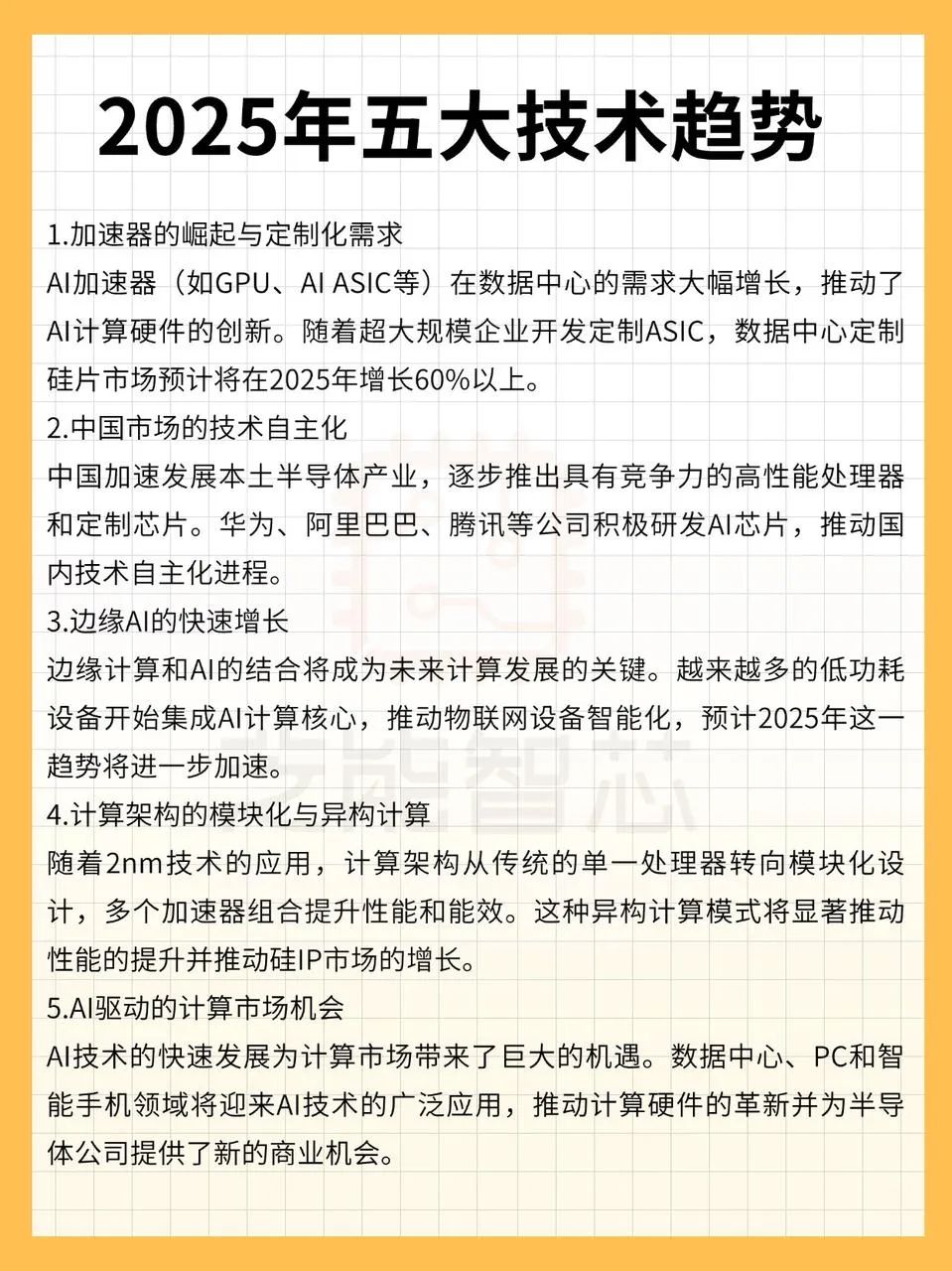

According to the latest report, the computing field is poised to witness several pivotal trends by 2025, encompassing the rise of accelerators, the independent growth of the Chinese market, competition for cutting-edge technologies, the development of future computing architectures, and the intelligence of IoT.

These trends not only mirror the rapid evolution of computing hardware and software technologies but also underscore shifting market demands. Let's delve into these trends and analyze their implications for the future of the computing industry.

Part 1

Computing Power Enhancement and Market Transformation

● The Race for AI Accelerators

The rapid advancement of AI chips is profoundly transforming the computing landscape. During AI training and inference, the demand for specialized accelerators (such as GPUs, AI ASICs, and HBM controllers) has soared. By 2024, revenues from AI accelerators in data centers doubled, and it is anticipated that related revenues will continue to climb through 2025.

NVIDIA has consolidated its dominant position with the Blackwell series, maintaining a GPU market share exceeding 96%, while AMD faces challenges in disrupting the market due to a lack of robust ecosystem support.

Custom ASIC chips have emerged as a new growth area for hyperscale enterprises. Google's sixth-generation TPU, AWS Trainium, and Microsoft's Cobalt chips are tailored for specific AI workloads, driving a 60% increase in market size by 2025.

Companies like Broadcom and Marvell have emerged as significant beneficiaries of this race, leveraging their mature IP and packaging technologies.

The computing field is shifting towards high customization and specialization, with innovations from hyperscale enterprises continuously reshaping the market landscape!

● Evolution of Computing Architectures

The evolution of computing architectures is moving towards modularity and flexibility. In 2024, fabless companies accounted for over 50% of the global semiconductor market, marking a transition from integrated to modular processor design.

Advancements in advanced packaging technologies and chiplets enable the flexible integration of different computing modules, thereby enhancing overall performance and energy efficiency.

In 2025, with the implementation of 2nm technology, the computing field will enter a new phase of development.

Microprocessors are gradually evolving from traditional general-purpose solutions to systems composed of multiple accelerator modules. This heterogeneous computing model can significantly enhance processing capabilities and efficiency.

This trend has not only fueled rapid growth in the silicon IP market but also opened up new avenues for companies like Broadcom and Marvell.

Part 2

Geopolitical Shifts and Terminal Intelligence

Amid the dual impact of US export restrictions and local policy support, China's semiconductor industry has reached a critical juncture. Due to geopolitical shifts and trade restrictions, China is accelerating its pursuit of technological independence, especially in the semiconductor sector.

By 2025, China is anticipated to gradually develop competitive high-performance processors and customized chips, transitioning from previously low-end processors. Chinese tech giants (such as Huawei, Alibaba, Tencent, and Baidu) are rapidly ascending in the AI realm.

China will place greater emphasis on local chip research and development, not only presenting new opportunities for domestic manufacturers but potentially altering the competitive dynamics of the global semiconductor industry. Huawei's chips manufactured through SMIC have already secured a notable market share in the data center sector, laying the groundwork for further advancement in China's semiconductor industry.

As AI migrates from the cloud to the edge, microcontrollers (MCUs) are integrating NPUs and low-power AI cores.

The Internet of Things (IoT) is swiftly integrating AI technology, evolving towards smarter devices. By 2025, IoT devices are expected to incorporate enhanced edge computing and AI processing capabilities, particularly in low-power devices.

Companies like ST Micro, Renesas, Microchip, and NXP have already introduced MCUs with built-in NPUs, providing intelligent computing capabilities for IoT devices.

IoT devices are increasingly equipped with AI computing cores, and edge computing will become the cornerstone platform supporting AI applications. These smart devices will offer users more efficient intelligent experiences through precise data processing and real-time responses.

● Manufacturers such as ST and NXP have launched MCUs that support edge inference, while Arm's Ethos series IP further propels the adoption of RISC-V architecture in low-power scenarios.

◎ The popularity of the NVIDIA Jetson platform has spurred the penetration of AI computing power into niche areas like industrial control and smart homes.

◎ The hardware competition has intensified, with Intel introducing its first AI PC chip, Copilot, and AMD capturing the market with Ryzen AI Max+.

◎ Qualcomm and Apple are deploying in the mobile space, aiming to set new standards for AI phones through TOPS (Tera Operations Per Second) metrics.

In this competitive landscape, energy efficiency has surpassed pure computing power as the decisive factor. The launch of NVIDIA's low-power chips signifies a leap from 'usable' to 'user-friendly' for edge AI.

It is anticipated that by 2025, competition around platform TOPS (Tera Operations Per Second) will intensify, necessitating continuous improvement in the optimization capabilities of diverse computing engines (including NPUs, GPUs, and CPUs).

The latest offerings from AMD and NVIDIA will deliver groundbreaking AI performance, especially in terms of power consumption optimization and computing efficiency. The momentum behind edge AI is robust, gradually supplanting traditional processors to emerge as a prominent force in the computing field.

Summary

The global chip industry in 2025 stands at the intersection of technology and market dynamics. AI-driven computing power enhancements, geopolitically fueled localization demands, and the wave of terminal intelligence are collectively shaping a novel industry landscape.

-

![]()

DeepSeek Ignites AI Mobile Phone Market, Stirring Up Waves in SoC Industry

-

![]()

Hisense Air Conditioners Embrace the 'New Wind' of Market Trends for 18 Years

-

![]()

JD.com and the Quest to Disrupt the Food Delivery Duopoly

-

![]()

Is Deepseek Truly a Source of Anxiety for Jiangsu?

-

![]()

OPPO Unveils New Foldable Phone Starting at 8999 Yuan, Aiming to Rival Huawei and Samsung

-

![]()

Who Reigns Supreme in Profitability Among AI Glasses' Core Component Enterprises?

-

![]()

Revolutionizing Edge AI: DeepSeek Paves the Way for Real-World Implementation

-

![]()

Unveiling Apple's Dual Strategies with the iPhone 16e