How Did Didi Quietly Thrive in the AI Era?

04/02 2025

04/02 2025

558

558

Since its listing in the United States, Didi has adopted a more low-key approach. Despite the proliferation of AI and the popularity of Chinese concept stocks, this internet giant seems to be rarely mentioned in the market.

However, in terms of share price, it has been steadily rising over the past two years.

Coincidentally, Didi recently released its Q4 2024 and full-year financial results. Judging from the report, while maintaining a low profile, the company has not had an easy journey.

I. Turning Losses into Profits

Didi's business model is straightforward. Its core lies in platform-based operations, leveraging big data and intelligent algorithms to precisely match the supply and demand of drivers and passengers, thereby improving operational efficiency, reducing empty driving rates, and providing convenient travel services to users.

Since its inception, Didi relied on burning money to provide subsidies and gain market share. Losing billions annually was common, ultimately leading to a network effect and a monopoly position (over 70% market share).

By connecting a massive number of drivers and passengers, Didi has built a robust travel ecosystem. In this model, the stable travel mindset on the user side and the sticky driver supply on the supply side promote each other, creating a virtuous cycle. Meanwhile, with its powerful algorithmic capabilities, Didi continuously optimizes route planning and supply-demand matching, further enhancing operational efficiency and user experience, thereby solidifying its competitive moat.

However, after achieving a monopoly position, Didi was not seen making money, leading to market doubts. After all, Uber, its competitor, was making substantial profits.

Nevertheless, in the past two years, Didi has begun to quietly generate revenue. It speaks less but does more.

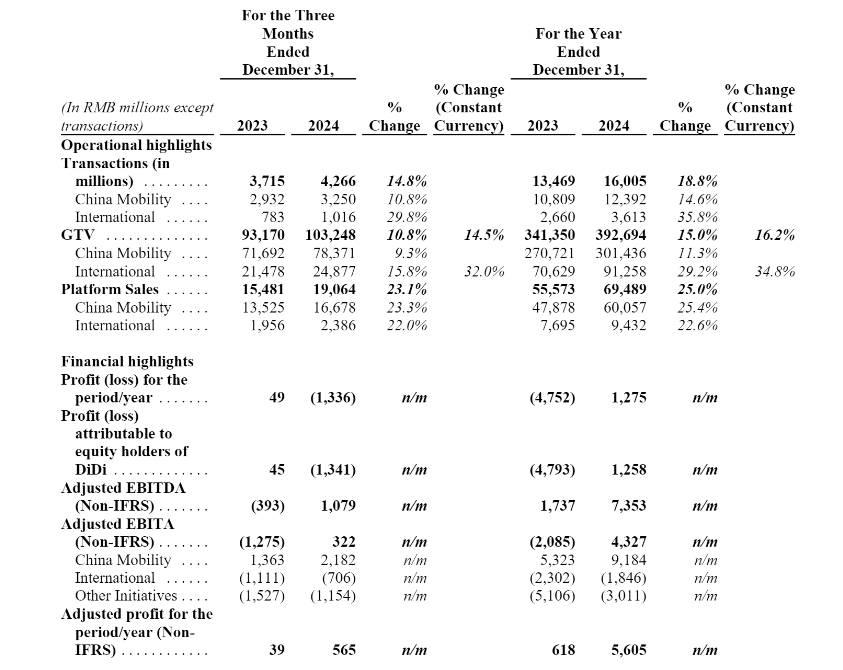

In 2024, Didi turned losses into profits. For the full year of 2024, Didi achieved revenue of 206.8 billion yuan, a year-on-year increase of 7.5%. It made a profit of 1.3 billion yuan, compared to a loss of 4.8 billion yuan in 2023; adjusted EBITA was 7.4 billion yuan, up from 1.7 billion yuan in 2023.

However, looking solely at the fourth quarter, profitability fluctuated slightly, with the first three quarters performing relatively better. Fourth-quarter revenue increased by 7.1% year-on-year to 52.9 billion yuan, with a loss of 1.3 billion yuan for the quarter, compared to a profit of 49 million yuan in the same period of 2023; adjusted EBITA was 1.1 billion yuan, up from 400 million yuan in the same period of 2023.

In terms of operational data, Didi's core platform order volume reached 16.005 billion orders in 2024, a year-on-year increase of 18.8%, with total transaction value (GTV) exceeding 392.7 billion yuan, a year-on-year increase of 16.2%. In the fourth quarter of 2024, Didi's core platform transaction volume reached 4.266 billion orders, a year-on-year increase of 14.8%. The core platform GTV reached 103.2 billion yuan, a year-on-year increase of 14.5%. In the fourth quarter, the number of travel orders in China increased by 10.8% year-on-year to 3.25 billion orders, with a quarterly average daily order volume exceeding 35.3 million orders, a record high.

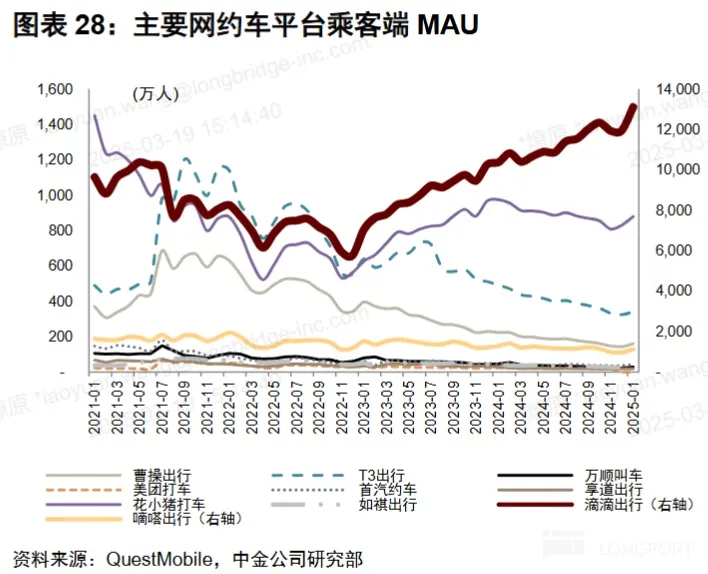

From the overall platform transaction volume and GTV, it is evident that the platform's transaction volume has grown significantly. Didi should continue to solidify its monopoly position in the online ride-hailing market. According to third-party research on user-end App MAU data from late 2024 to early 2025, the monthly active users of Didi and its subsidiary Huaxiaozhu App have increased significantly, suggesting an improved market share.

However, the substantial growth in GTV compared to revenue and profitability indicates that competition remains fierce, and Didi may have increased subsidies.

Especially when analyzing domestic and international segments separately, we can see the differences between the two markets.

The Chinese market, as the base, recorded a full-year order volume of 12.392 billion orders, a year-on-year increase of 14.6%, with GTV reaching 301.4 billion yuan. It achieved incremental breakthroughs through diversified services beyond traditional ones like online ride-hailing, taxis, and ride-sharing. The expansion into niche scenarios such as intercity buses, pet taxis, and chartered buses not only increased user stickiness but also opened up high-margin market space. In the fourth quarter, the average daily order volume for travel in China reached 35.3 million orders, achieving GTV of 78.4 billion yuan, a year-on-year increase of 9.3%, indicating that there is still room for growth on the demand side.

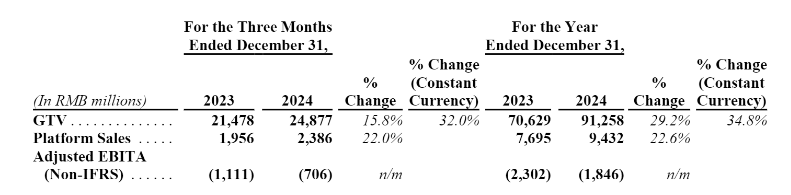

International business became a significant highlight, with a full-year order volume of 3.613 billion orders, a surge of 35.8% year-on-year, and GTV reaching 91.3 billion yuan, with a growth rate of 34.8%. The continuous investment in the Latin American market (Brazil, Mexico) has yielded substantial results, with GTV growth exceeding 30% for four consecutive quarters and achieving adjusted EBITDA profitability in 2024. The success in the Latin American market has the potential to be replicated in other markets. Excluding exchange rate factors, the GTV growth rate of the international business in the fourth quarter still reached 32%, with no significant slowdown.

While the domestic market environment seems large with high demand, it actually has even greater supply and fierce competition. As of 2024, the number of online ride-hailing drivers nationwide exceeded 6 million, more than doubling since the beginning of 2021. Competitors include aggregation platforms like Gaode, Meituan, and Ctrip. Many of the most lucrative airport taxi scenes have been taken over by Ctrip. Additionally, there are price controls and well-established infrastructure for other modes of transportation, so people do not necessarily choose taxis.

In contrast, the overseas market may be much more promising, with less competition and less developed infrastructure. There are limited transportation options available, and most people rely on driving. As long as it is cheaper than taxis, there is significant potential for profit. The profitability and imagination in overseas markets are higher than those in the domestic market.

Whether it is the total transaction volume or the breakthrough in single-day order volume, Didi should have recovered from the previous delisting crisis. At the same time, it has become increasingly low-key because although it has begun to generate revenue, it is still not easy, and the domestic market remains the main battleground.

II. A Low-Key Breakthrough with All-in on Autonomous Driving

Didi previously enthusiastically entered group buying and car manufacturing but has now actively retreated from the group buying business and sold its car manufacturing business, contributing to the group's profitability through cost reduction and efficiency enhancement.

With these businesses no longer operational, what is Didi's future narrative?

It can only be All-in on autonomous driving.

Relying on its ecological network of tens of millions of daily orders, Didi has an advantage over car manufacturing enterprises or other internet companies like Baidu if its autonomous driving reaches a level where it can massively develop driverless taxis. Its order demand already exists, and the number of users plus corresponding scenarios and usage habits have already given Didi a network effect. Adding the Robotaxi option is straightforward, as the market scenarios are the same, and only the demand customers need to be segmented. With a large user base and multiple runs, the daily operating cost is extremely low, reportedly at 1.2 yuan per kilometer, only 40% of that of fuel vehicles.

China International Capital Corporation predicts that by 2030, the global Robotaxi market size will exceed 2 trillion US dollars, significantly surpassing the online ride-hailing market. Automotive consulting service agency IHS Markit also predicts that by 2030, the total market size of shared travel in China will reach 2.25 trillion yuan, of which Robotaxi will account for 60%, or 1.3 trillion yuan. Robotaxi may be the ultimate solution to urban travel.

As early as 2021, Didi listed autonomous driving as one of its core strategic segments in its prospectus. Now, after selling its car manufacturing business to Xiaopeng, it only retains Andi Technology, a joint venture with GAC Aion, with a more focused direction.

Unlike its past ventures, Didi has been very low-key about autonomous driving. Moreover, it is incubated externally, allowing for continuous capital financing.

In 2020, it obtained over 500 million US dollars in financing led by SoftBank Vision Fund.

B round in 2021: IDG Capital, CPE, Paulson, China-Russia Investment Fund, Guotai Junan International, and CCB International.

B+ round in 2022: Mubadala Investment Company of Abu Dhabi.

C round in 2023: GAC Group.

Recently, it was revealed that Didi's autonomous driving company is seeking a new round of financing with a target valuation of approximately 5 billion US dollars.

Compared to the high-profile road tests of companies like Baidu Apollo and Pony.ai, Didi only mentioned that its Robotaxi has "mixed dispatching in demonstration areas in Beijing, Shanghai, and Guangzhou, with continuous safe operations exceeding 1500 days."

After experiencing absolute power, silence may be a safe strategy for Didi.

However, there are also other developments.

In April 2024, Andi Technology, a joint venture between Didi Autonomous Driving and GAC Aion, received approval for its business license and will launch its first mass-produced L4 model in 2025.

At the same time, there were personnel adjustments within Didi. In December, Didi internally announced that it had approved Zhang Bo's application to step down as the group's CTO, and that Zhang Bo would focus on the autonomous driving business in the future. Zhang Bo will continue to serve as a member of the group's class committee and CEO of the autonomous driving company.

Although Didi's autonomous driving has been low-key for a long time, it is highly likely to reach the stage of commercial launch in the next two years.

Conclusion

Through strategic retreat and refined operations, Didi has gradually emerged from the shadow of the 2021 security incident. The 2024 financial report demonstrates its resilience in mature markets and potential in emerging markets. At the same time, Didi has strengthened investor confidence through share repurchases. The 1 billion US dollar repurchase plan initiated in 2023 has completed 850 million US dollars, and a new 2 billion US dollar plan was approved in March 2025.

Autonomous driving carries the core imagination space for Didi's future growth. Although Didi still dares not be high-profile about its progress in AI or autonomous driving, from the clues, it is evident that Didi is going all in.

Despite facing multiple challenges, with its data advantages and scenario synergy, Didi is still expected to occupy an important position in the Robotaxi race.

-

![]()

Reevaluating vivo's Leap into Robotics

-

![]()

iOS 18.5 In-depth Review: Does Apple's Latest Update Cater to Chinese Users?

-

![]()

Qingming Holiday Spurs Demand Surge! Will Hitchhiking Become the Next 100 Billion Travel Market?

-

![]()

Samsung S25 Claims the Title of the Price Drop King in 2025, Outpacing iPhone 16e

-

![]()

Unisound AI Races to Hong Kong IPO with Estimated Valuation of RMB 9 Billion

-

![]()

QuantGroup Garners Broad Market Acclaim, Recently Pursuing IPO

-

![]()

California Startup Unveils Groundbreaking Optical Interconnect Technology to Revolutionize AI Computing

-

![]()

European Auto Market | March 2025: Spain Records 23.2% YoY Surge in Car Sales