Xiaomi Q4 Report: Outshining Tesla with Robust Performance

03/19 2025

03/19 2025

494

494

A 70% increase since the beginning of the year is overshadowed by Xiaomi's exceptional performance in this financial report.

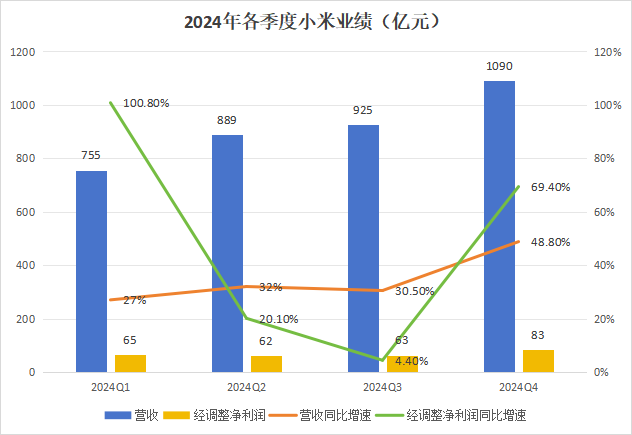

Let's delve into the financial report data and compare it with expectations. In Q4, Xiaomi recorded revenue of 109 billion yuan, marking a 48.8% year-on-year increase and setting a new record for the company's single-quarter revenue. Market consensus was 104.38 billion yuan, while adjusted net profit stood at 8.316 billion yuan, representing a 69.4% year-on-year increase, surpassing market expectations of 6.54 billion yuan by a significant 14.3%. As Lei Jun noted, this is Xiaomi's "strongest annual report ever".

From Xiaomi's financial report, we have identified several core messages that warrant attention:

First, Xiaomi has decisively proven its ability to achieve exceptional growth. Notably, the growth rate of adjusted net profit significantly outpaces that of revenue, both achieving double-digit growth. With the exception of Q1 2024, which saw a 100% adjusted net profit growth rate due to a particularly low baseline in Q1 2023 following the recent easing of restrictions, Q4 set a new record for Xiaomi's revenue and adjusted net profit growth over the past year.

Second, the company has successfully cultivated its own growth driver—premiumization. From a consumer perspective, those who can afford cars priced above 200,000 yuan are considered high-end consumers. The overwhelming success of Xiaomi Su7 has effectively opened the door for the entire Xiaomi ecosystem to embrace premiumization. Traditional valuation methodologies and forecasting logics are no longer adequate to predict Xiaomi's performance.

This disparity is evident in the market's expectations. Despite the market consensus already pricing in Xiaomi's Q4 performance, the company still delivered impressive growth. Especially in terms of adjusted profit, the market underestimated the actual figure by 14.3%, indicating the failure of old valuation logic.

Finally, with a market capitalization of 1.45 trillion Hong Kong dollars as of March 18th's closing, divided by Xiaomi's full-year adjusted net profit of approximately 29.3 billion Hong Kong dollars, the company's current adjusted PE ratio stands at just over 49 times. In contrast, even after recent declines, Tesla's PE ratio remains over 100 times. Given Xiaomi's impressive performance, it is difficult to argue that the company is currently "overvalued" by the market.

01 Reconstructing Valuation Logic

The reconstruction of Xiaomi's valuation system must begin with its auto business.

Many are puzzled by the sudden surge in Xiaomi Su7 sales. It's crucial to understand that this is not due to an increase in the number of people who can afford cars priced above 200,000 yuan, leading to a "consumption upgrade" in the automotive sector. Rather, it's because those who previously considered buying performance cars priced above 300,000 yuan have chosen to "downgrade" their consumption. In other words, Xiaomi has captured a significant portion of the market share from traditional fuel vehicles priced between 300,000 and 400,000 yuan.

Broadly speaking, the "consumption downgrade" demand of China's affluent population supports most current mid-to-high-end new energy vehicles and automakers, driving a restructuring of the automotive industry. We believe this trend is unlikely to change in the short term and will likely deepen at least until 2025.

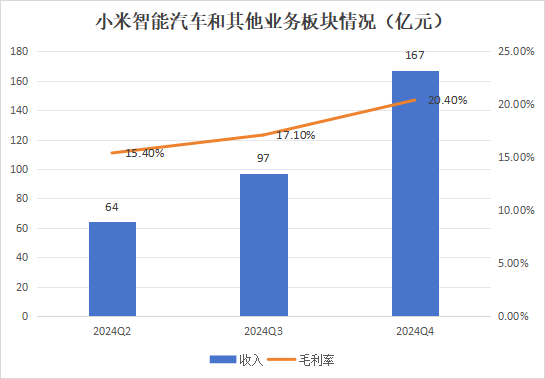

Regarding Xiaomi's auto business performance, the financial report reveals that in 2024, the company's smart car and other business revenue reached 32.8 billion yuan, with smart car revenue accounting for 32.1 billion yuan, comparable to Xpeng, which reported full-year auto sales revenue of 35.8 billion yuan. In Q4, Xiaomi's auto revenue hit 16.3 billion yuan, with an adjusted net loss of 700 million yuan.

It's worth noting that Q4 was the first quarter to disclose the adjusted net loss for the smart car business segment. However, based on the full-year adjusted net loss of 6.2 billion yuan for this segment, the net loss in Q4 should have narrowed significantly on a sequential basis. Additionally, Xiaomi discloses the gross margin of smart cars every quarter. Starting from Q2, Xiaomi's car gross margins were 15.4%, 17.1%, and 20.4%, respectively, with a full-year comprehensive gross margin of 18.5%.

The 20.4% gross margin in Q4 alone is unprecedented, a feat achieved by few new-energy vehicle companies in their first year of vehicle launch. Compared horizontally, Xiaomi's gross margin is comparable to renowned automakers like BYD and Li Auto, surpassing both Tesla and Xpeng. It's fair to say that Xiaomi starts at a first-class level. Even when compared with top-tier fuel vehicle companies such as Toyota and Volkswagen, Xiaomi's gross margin ranks among the best.

Of course, we recognize that many eagerly await Xiaomi's auto business to turn a profit on an adjusted basis, but honestly, this is not their top priority at the moment.

First, according to founder Lei Jun's projections, Xiaomi's annual delivery target for 2025 has been increased to 350,000 units, implying greater production capacity, more models, and consequently, more investment. To build on the success of the Su7, Xiaomi's auto business cannot afford to slacken amid the intensifying competition in the new energy vehicle market. Fluctuations in adjusted net profit over the next few quarters are likely, and even if losses expand, it doesn't necessarily signify negative news for Xiaomi.

Second, some may argue that Xiaomi's soaring accounts payable indicate that the company's true operating conditions have not fundamentally improved. However, given Xiaomi's already strong position in the supply chain and its expansion into the auto business, it would be odd if accounts payable did not increase. For a company with triple manufacturing identities in mobile phones, Internet of Things (IoT) consumer products, and smart cars, and given that these sectors are not blue oceans in a commercial sense, achieving today's results is not a given but a remarkable achievement.

Finally, the merit of Xiaomi's auto business lies in broadening the company's user base to include those with the ability to consume cars priced above 200,000 yuan, encompassing high-net-worth female consumer groups that Xiaomi has not previously reached. The consumption potential of this group is not fully reflected in this financial report and still holds considerable growth potential in the coming quarters.

Therefore, taken together, no consumer electronics company in the world has achieved what Xiaomi has today. While Xiaomi may not be "top-tier" in various aspects, this does not diminish the fact that its valuation logic is evolving.

02 One Regret and One Expectation Gap

If we were to nitpick Xiaomi's 2024 business, AI might be one area of concern.

In 2024, the spotlight was predominantly on Lei Jun and the Su7, with other products, especially consumer electronics integrated with AI, lacking prominent highlights. In fact, Xiaomi boasts the most comprehensive AI application scenarios among all Chinese enterprises, encompassing mobile phones, cars, PCs, tablets, and various home appliances. However, the lack of highlights in AI integration across these scenarios easily recalls a significant misstep Xiaomi made in its early days: MiTalk.

At that time, Lei Jun misjudged the development progress of its competitor WeChat, resulting in MiTalk, which Xiaomi had launched first, being overshadowed by the times. In 2025, Lei Jun must place greater emphasis on narrating the story of AI integration within Xiaomi. As the brand enters the premium market, leveraging AI to enhance product value will be beneficial for both consolidating established consumer perception and future price increases.

At the earnings meeting, Xiaomi Group President Lu Weibing stated that Xiaomi will invest approximately 1/4 of its total R&D budget, or roughly 7 billion to 8 billion yuan, in AI. In the long run, AI, OS, and chips are listed as Xiaomi's core technologies. In the short term, Xiaomi needs to build a robust AI infrastructure, develop AI technologies such as large language models and multimodal large models, and establish application scenarios for deploying large AI models, including Super Xiaoai, smart cabins, and intelligent driving. Xiaomi will also utilize AI technology internally to improve efficiency.

Having discussed the regret, let's conclude with the expectation gap. Many overlook an important technology Xiaomi is currently developing, which has been criticized by the outside world—chips. In 2024, a piece of news was overlooked by the entire internet, documenting Xiaomi's phased achievements in core chip technology development. Based on objective laws, it won't be long before Xiaomi achieves a major breakthrough in chip development.

For a consumer electronics company spanning multiple fields, possessing its own chip research and development capabilities is a remarkable achievement, representing the deepest divide between "technology companies" and "manufacturing companies." The market is reassessing Xiaomi's valuation by crossing this divide, but ultimately, Xiaomi itself needs to deliver, allowing the market to recognize its chip design capabilities.

Looking back, just like after the sudden emergence of Xiaomi Su7, every day leading up to substantial progress in chip research and development is a golden opportunity.

Disclaimer: This article is for learning and exchange purposes only and does not constitute investment advice.

-

![]()

Dianping Merges into Core Local Business as Meituan Advances Towards Greater Unity

-

![]()

Reevaluating vivo's Leap into Robotics

-

![]()

iOS 18.5 In-depth Review: Does Apple's Latest Update Cater to Chinese Users?

-

![]()

Qingming Holiday Spurs Demand Surge! Will Hitchhiking Become the Next 100 Billion Travel Market?

-

![]()

Samsung S25 Claims the Title of the Price Drop King in 2025, Outpacing iPhone 16e

-

![]()

Unisound AI Races to Hong Kong IPO with Estimated Valuation of RMB 9 Billion

-

![]()

QuantGroup Garners Broad Market Acclaim, Recently Pursuing IPO

-

![]()

California Startup Unveils Groundbreaking Optical Interconnect Technology to Revolutionize AI Computing