Kuaishou Grapples with Growth Stagnation: Mini-drama Sector Faces Anxiety, AI Commercialization Prospects Uncertain

04/02 2025

04/02 2025

433

433

Recently, Kuaishou (01024.HK) released its full-year 2024 financial report, revealing a noticeable slowdown in the growth rate of its core business segments.

Stockstar observed that the mini-drama sector, which Kuaishou has heavily invested in, is now confronted with fierce competition and escalating content homogenization. Relying solely on the mini-drama business is proving insufficient to reverse the company's growth challenges in its pillar businesses and its plateauing user base. Additionally, the growth rate of e-commerce GMV (Gross Merchandise Volume) has been declining consecutively, hindering the development of the company's internal advertising business.

Furthermore, the company's video generation large model, Keling AI, despite being a focal point of external attention, generates minimal revenue, sparking doubts about its commercialization prospects in the market.

Pillar Businesses Struggle to Boost Revenue, User Growth Hits a Ceiling

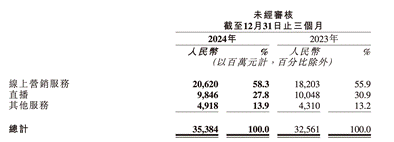

The financial report indicated that in 2024, Kuaishou achieved operating revenue of 126.9 billion yuan, a year-on-year increase of 11.8%; adjusted profit was 17.7 billion yuan, up 72.5% year-on-year. In Q4, the company's total revenue was 35.4 billion yuan, a year-on-year increase of 8.7%, with adjusted profit reaching 4.7 billion yuan, up 7.8% year-on-year.

Regarding business segments, online marketing services (advertising) are Kuaishou's primary revenue source, contributing over 50% of the company's total revenue.

The company classifies its online marketing services into external cycle advertising revenue and internal cycle advertising revenue. External cycle marketing customers drive the growth of online marketing service revenue. In the financial report, Kuaishou acknowledged the contributions of the content consumption industry, including mini-dramas, mini-games, and novels, stating that the marketing consumption of commercialized mini-dramas surged by over 300% year-on-year in Q4.

Stockstar noted that Kuaishou has been actively expanding its mini-drama market in recent years. In January last year, the company introduced an upgraded Kuaishou "Xingmang Mini-drama" cooperation plan to support high-quality mini-dramas. Later, in October, Kuaishou launched a new online cooperation model, the distribution matchmaking recruitment model, which shortened the communication gap between copyright owners and distributors, optimized the operational efficiency of the mini-drama industry, and thereby fueled the growth of the mini-drama business.

Simultaneously, the company launched a new model for commercial monetization. At the end of last year, Kuaishou introduced a "paid mini-drama membership" in addition to the existing IAP (in-app purchase) and IAA (in-app advertising) models.

However, with the entry of platforms such as iQIYI, Tencent, Baidu, Pinduoduo, and Xiaohongshu, competition in the mini-drama market has intensified, content homogenization has become more pronounced, and user aesthetic fatigue is emerging. In March this year, Kuaichuang, a mini-drama company under Ying Universe, issued a warning letter to Kuaishou's mini-drama APP Xifan, alleging unauthorized shelving and distribution of multiple copyrighted works, infringing on Kuaichuang's intellectual property rights. This incident underscores Xifan's anxiety in the realm of content creation, particularly concerning originality.

Performance-wise, the mini-drama business has failed to reverse the slowdown in the company's online marketing service growth. In 2024, Kuaishou's online marketing service revenue was 72.419 billion yuan, a year-on-year increase of 20.09%, compared to a growth rate of 22.97% in 2023. Specifically, Q4 business revenue was 20.6 billion yuan, up 13.3% year-on-year, a significant drop from the 55.9% growth rate in the same period of 2023.

In terms of user scale, in 2024, Kuaishou's average daily active users (DAU) and average monthly active users (MAU) reached 399 million and 710 million, respectively, with year-on-year growth rates of 5.13% and 4.64%. In 2023, DAU and MAU growth rates were 6.8% and 10.69%, respectively, both decelerating. This indicates that relying on the mini-drama business alone is challenging for the company to break through the current user growth ceiling.

E-commerce GMV "Decelerates", Live Streaming Business Contracts

Stockstar observed that as user growth peaks, Kuaishou's e-commerce GMV growth is sluggish. From 2021 to 2024, Kuaishou's e-commerce GMV amounted to 680 billion, 901.2 billion, 1.1844 trillion, and 1.3896 trillion yuan, with year-on-year growth rates of 78%, 33%, 31%, and 17%, respectively.

Reflecting on revenue, the growth rate of other service revenues, inclusive of e-commerce, has also shown a deceleration trend. In 2024, Kuaishou's other service revenue was 17.4 billion yuan, a year-on-year increase of 23.4%, lower than the 44.7% growth rate in 2023.

Kuaishou has established a commercial closed loop centered on its e-commerce business. Industry insiders view e-commerce as the driving force behind the growth of internal advertising, as internal advertising primarily stems from investments by merchants or broadcasters within the platform who pay for exposure. Therefore, the decline in e-commerce GMV growth will not only directly impact the growth of e-commerce commissions but also affect its internal advertising and e-commerce buying within its live streaming business.

Strategically, Kuaishou's e-commerce is evolving towards "omnichannel management," with store operations as the core, driven by a dual cycle of "self-broadcasting + distribution," focusing on content seeding fields centered on "short videos + live streaming" and pan-shelf fields centered on "search + mall".

However, industry insiders pointed out that content platforms, exemplified by Kuaishou, lack a category advantage when deploying shelf e-commerce. Traditional e-commerce platforms have long cultivated user perceptions through their advantageous categories, such as Tmall's dominance in clothing and beauty, JD.com's focus on self-operated 3C and home appliances, and Pinduoduo's concentration on agricultural products and daily necessities.

The live streaming business was once Kuaishou's most recognizable feature, but it has continued to shrink. For the full year of 2024, the company's live streaming revenue was 37.1 billion yuan, a year-on-year decrease of 5.1%, with Q4 live streaming revenue at 9.8 billion yuan, down 2% year-on-year, marking a decline for four consecutive quarters.

Although Kuaishou continues to build head categories like multi-person live streaming, group live streaming, and live streaming stages, explore and support locally grown small and medium-sized broadcasters, and jointly conduct dual-platform live streaming business with Huya, the decline in this business persists.

Behind this trend, on the one hand, the live streaming industry has witnessed stricter regulations in recent years, with rigorous governance over vulgar, sensational, and non-compliant content, which has somewhat constrained the business's development. On the other hand, the online live streaming industry as a whole has matured, and intra-industry competition remains intense.

Keling Commercialization Faces Hurdles, Overseas Profitability Issues Persist

Stockstar noted that Kuaishou's video generation large model, Keling, is considered a highlight of this financial report by the outside world. Keling was officially launched in June last year and has since released version 1.6, with significant improvements in semantic compliance, visual aesthetics, and dynamic quality.

The company mentioned in the financial report that the commercialization of Keling AI has shown a trend of steady acceleration. Since the commencement of commercialization, as of February this year, the cumulative operating revenue has surpassed 100 million yuan. However, currently, the revenue generated by Keling AI constitutes less than one thousandth of Kuaishou's annual revenue.

Following the launch of Keling, numerous companies have also introduced similar products, such as ByteDance's "Jimeng AI" and Minimax's "Conch AI." Compared to similar products on the market, according to a research report by China Merchants Securities, overseas YouTube bloggers compared products like Conch AI, Runway, and Keling AI. The results indicated that Conch AI significantly leads in motion generation, especially regarding the smoothness and realism of human movements, outperforming competitors like Runway and Luma AI.

Moreover, the market harbors doubts about the commercialization prospects of Keling.

On the one hand, compared to models that generate images from text, which have already found stable applications in fields like advertising and content creation, the practical application scenarios of large video generation models still have certain limitations, and user demand for AI video generation has not been fully unleashed. On the other hand, industry insiders believe that there is considerable uncertainty surrounding Keling's profitability prospects. The training cost of large video models is high, and it remains unclear whether Keling's profits can cover hardware costs.

Apart from AI, Kuaishou is also accelerating its overseas expansion.

At the Kuaishou Overseas Commercialization Greater China 2025 Kick-off Conference held in March this year, the head of Kuaishou International Commercialization announced that the company will continue to prioritize "going overseas + AI." It is understood that in terms of overseas business, Kuaishou has chosen to deeply embed itself in the Brazilian market, and the company's head stated that Kwai has become a national-level content social platform in Brazil.

In terms of performance, although Kuaishou's overseas revenue has increased, it still faces profitability challenges. In 2024, the company's overseas revenue was 4.696 billion yuan, a year-on-year increase of 105.6%, accounting for less than 5% of total revenue. Meanwhile, the company's operating loss was 934 million yuan, and it has yet to achieve profitability. (This article was originally published on Stockstar, Author|Li Ruohan)

- End -

-

![]()

Tech Giant's Next Leap: Is the Ultimate Goal of Car Manufacturing Robot Building?

-

![]()

"Post-00s" Rush for Spring Recruitment, Navigating the AI-Dominated Era

-

![]()

How did Great Wall Motors achieve high growth by breaking away from price wars?

-

![]()

Jaguar Land Rover Issues Passive Recall of 740,000 Vehicles in Two Months; China Sales Plummet 58% in First Two Months

-

![]()

GPT-4o Mass-Produces "Hayao Miyazaki": Artists Collective Defense Against AI-Driven Creativity

-

![]()

The Triumvirate of Gamepixel's Growth: Empowering Self-Development, Strengthening Platforms, and Leveraging AI Breakthroughs

-

![]()

April Fool's Special: AI Isn't as Smart as You Think

-

![]()

NIO's Letao has a new leader, is NIO closer to achieving its fourth-quarter profit target?